Can APIs Improve the Banking Customer’s Experience?

Hi there,

Banks are genuinely making a comeback in better CX. While many are improving their own channels, others are finding innovative ways to distribute their services on other platforms.

What’s the key technology element enabling this change for banks?

Can banks piggyback on others to take their products to market?

Will we see a world without physical bank branches?

Read on to find out.

Seshika Fernando

VP Banking and Financial Services,

WSO2

1. On the Comeback Trail!

Pre-pandemic, if you were having a great banking experience, it was likely from a “neo” or “challenger” bank. But the shift of gears on digital by incumbent banks during the pandemic was dramatic.

“An incumbent took first place, and the top 10 comprised 3 incumbents, 6 credit unions, and 1 challenger.”

Some banks (and credit unions) have upped the ante and even surpassed the CX standards of challenger banks; a task no doubt involving many unenviable hours of fighting layers of legacy tech and siloed data and functionality.

APIs have been the key driver, helping banks pull data and services out of this mix to enable seamless customer interaction.

2. Do Banks Really Need Physical Channels?

The shift to digital banking has rendered the geography of banks less relevant to their reach. Even the minority of branch dependent consumers have upgraded to phygital (using both digital and physical branches).

So, should banks do away with physical channels? Not really. S&P Global Market Intelligence shows how U.S. banks branch-closure rate is slowing down. This could signal that banks are starting to strike the balance between offering customers a mixture of physical locations and digital channels to conduct transactions.

“Physical channels have a great opportunity to be used as brand ambassadors focused on truly complex, empathy-centric situations.”

Does security always have to come at the cost of customer experience?

Historically, yes.

Example 1: Two factor authentication is always stronger, but it also means an additional hop for consumers before they log in.

Example 2: An extra verification (God forbid, OTP) prior to a high-value transaction might optimize fraud detection, but is definitely annoying for the consumer performing a genuine transaction.

It doesn’t have to be that way. Investing in tech-enabled strategies like ‘data-driven’ Customer Identity and Access Management (CIAM) can let banks and their customers have their cake and eat it too.

4. Looking Beyond ‘Own’ Channels

Digitization has enabled banking to be integrated into other industries. Banks are looking to reach more customers at a lower cost by embedding their services into non-financial websites, mobile apps, and business processes. a.k.a Banking as a Service (BaaS).

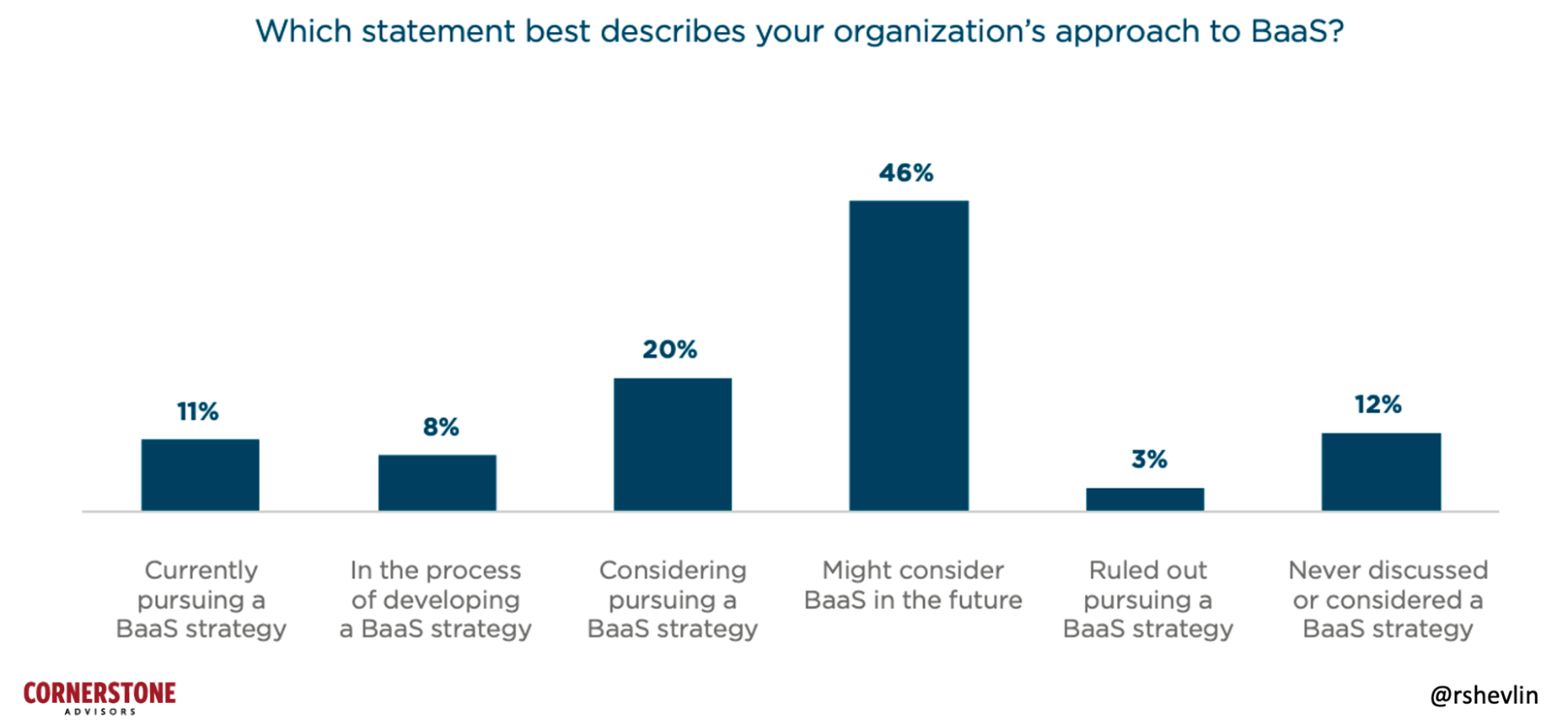

A recent report by Cornerstone Advisors found that 11% of banks already have a BaaS strategy, 8% are in the process of developing one, and 20% are considering it.

And what is enabling banks to embed themselves in this non-financial distribution network? APIs of course!

5. You Can’t Improve What You Don’t Measure

Just getting your API up and running isn’t going to help you with CX in the long run. How do banks know their efforts into creating an amazing CX is working?

NPS, CSAT, and CES scores are great for measuring CX improvements. But getting customers to fill these surveys may end up inconveniencing them, which you don’t want.

APIs help you measure what matters. If a bank is investing time and resources in uplifting their CX then they should be able to measure whether their customer’s experience has improved. And if so, how it’s reflected in its business metrics.

BBVA API Market shows how to measure these improvements under:

Performance metrics

User metrics

Engagement metrics

Business metrics

Featured Blog of the Month

Can Banks Leverage ‘Trust’ to Compete With Their Digital Competition on Providing Better Customer Experiences? read more

What did you think? Do you agree or disagree with my observations? Let me know by emailing [email protected]