My WSO2 colleague, CTO Eric Newcomer, recently suggested that fintech is in a “midlife crisis”. I don’t consider that a bad thing. Our industry is maturing, as it must. It is moving on from solving straightforward problems and taking on the immediate challenges. Now its intent is to find deeper solutions and to look for the non-obvious next steps.

It’s called mid-life because it’s the half where you bring experience and well-earned confidence to the project. This adds an exponential boost to your junior partners’ skill and enthusiasm. Now is the time for banks that are already digitizing – that is to say, all banks – to look forward with self-assurance to working with digital-native stakeholders.

Seshika Fernando

VP Banking and Financial Services, WSO2 LLC

1. Competition is Heating up: If you Can't Beat Them, Join Them

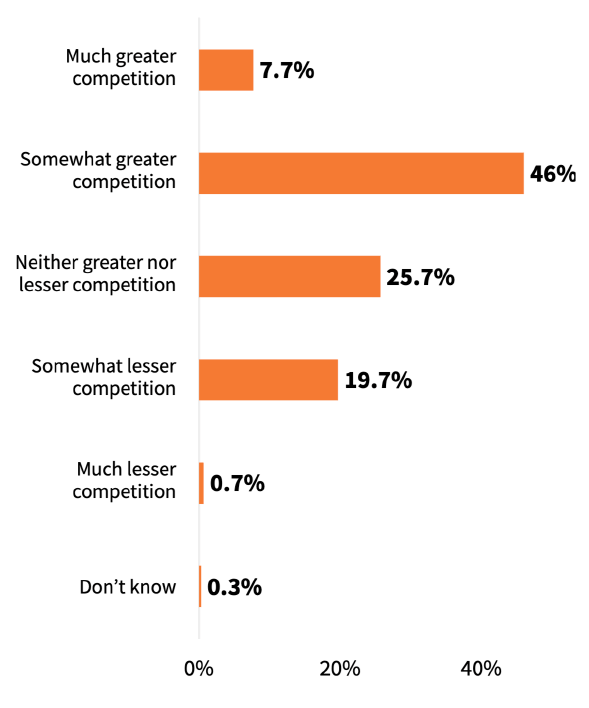

More than half of the respondents say their financial institutions have faced greater competition over the past three years from digital alternatives.

One reason is competition from non-financial – that is, non-regulated – firms such as technology giants and telecoms.

In your opinion, has your financial institutions faced greater or lesser competition over the past three years from digital alternatives?

“[T]hey can utilize data collected from various parts of their business whereas banks can primarily collect data through their financial services operations,” says Drew Propson of the World Economic Forum.

Conversely, increasing competition from fintechs was among the lowest rated reasons for greater competition, indicating they are being embraced as potential collaborators rather than competitors. Almost 50% of banks had partnered with fintech startups over the past three years.

2. ‘Unregulated’ Fintechs Aren’t Always at an Advantage

Of all the obstacles to improving digital services, the lowest-ranked was “too strict regulation,” not to be confused with third-from-the-bottom, “lack of regulation”.

So not only are fewer executives concerned about the onus of regulation, but the ones who do share that concern are divided over whether they need more or less of it. Corporate, not public, bureaucracy is much more of an impediment to innovation, the survey shows.

The key takeaways are: Institutions should support beneficial regulatory policies. Regulations can help to level the playing field in financial services by shining a light on the broader landscape, eliminating the grey areas inherent in forming partnerships between banks and non-banks.

3. Change the Culture, not Just the Vocabulary

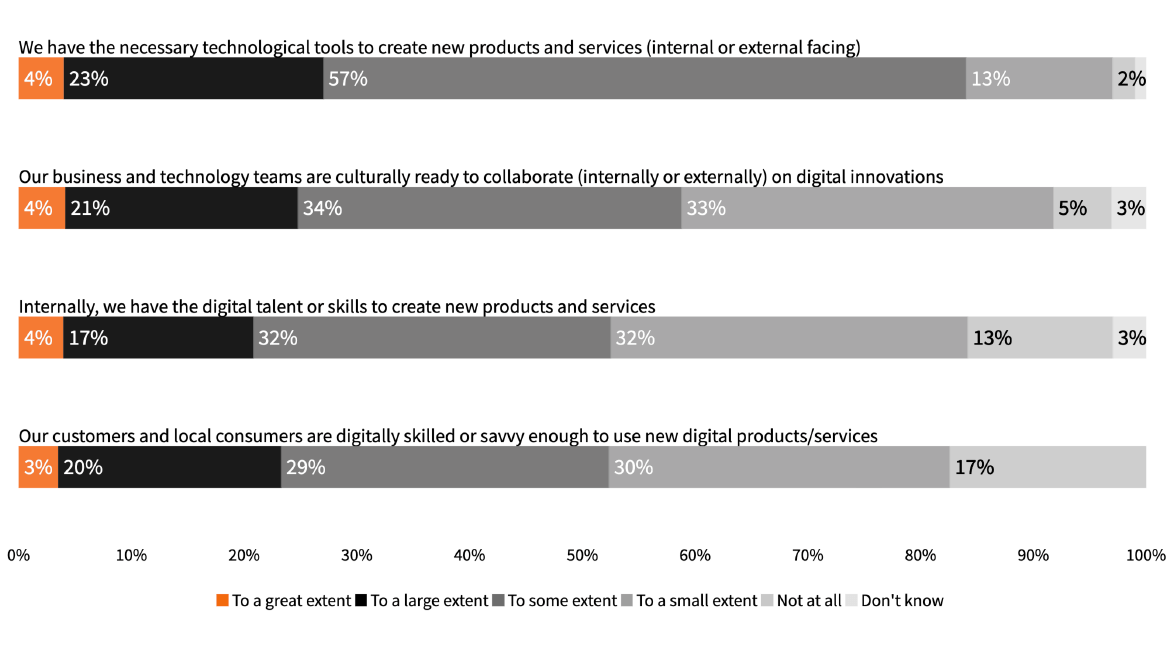

To what extent does your organisation have the necessary capabilities to create new digital products and services, and to what extent do customers have the skills or savvy them?

The greatest barriers to digital innovation, on the other hand, aren’t technological. According to the survey, banks have the tools. It’s the cultural readiness that’s the sticking point. That appears to be related to a lack of digital skills internally, which is in turn related to a lack of digital skills among the customer base. I’m not saying there’s necessarily a causal relationship here, but we can’t deny the correlation.

This finding is problematic. The cultural change required to take full advantage of digital transformation involves having a customer-centric view. You can’t then say that customers aren’t “savvy” enough to appreciate what you’re trying to do. If you’re not making banking easier for customers, then you’re doing digital transformation wrong.

4. People, People, People

Embracing cultural change throughout the organization was most frequently cited as an element adopted by financial institutions to counter growing digital competition. Other steps include hiring new staff to improve technology innovation and re-training or “upskilling” existing staff.

Maybe upgrading or refreshing people is more effective than upgrading or refreshing infrastructure.

“It is also important to futureproof employees by equipping them with digital skillsets,” says Jimmy Ng, CIO of DBS Singapore. “At DBS, we have trained over 18,000 employees in data skillsets, with about 2,000 of these upskilled in advanced areas of data science and business intelligence.”

The bank has previously collaborated with Amazon Web Services to launch the DBS DeepRacer League, a gamified method to train more than 3,000 employees, including senior leadership, in basic artificial intelligence and machine learning.

Banking has become a people-first, consumer-oriented business. Frankly, banking can no longer be the exclusive province of bankers, or at least of the familiar notion of bankers. Financial institutions can no longer compete with digital alternatives with the same old staff they had.

To start with, they must upskill their existing work force. Still, that in itself is insufficient. They must compete with fintechs in the recruitment arena, hiring top talent then providing the perks and innovative work environment to retain it.

5. Can Technology Save the Day?

Cloud? Internet of Things? Voice apps? Blockchain? Yesterday’s news. So is cybersecurity, surprisingly enough.

Big data and analytics, not so long ago the magic incantation that was supposed to inform every decision and make it flawless, is now in the middle of the pack, recognized by 18.7% of executives surveyed. It was edged out by augmented reality/virtual reality at 19.0%.

In third place was the granddaddy of technology solutions, business process automation at 21.3% The silver goes to mobile apps with 22.0% and the winner is AI at 24.3%.

Of course, technology can only be part of the solution. Executives from leading institutions are more likely to cite planning or executing broader cloud migration for technology systems as a key step to meet digital competition. They are also more open than laggards to creating partnerships and offering BaaS or embedded finance services to non-banking companies.

All this highlights the intensifying competition facing banks, but it also reveals how this competition is leading to unprecedented digital collaboration. Banks now accelerate their growth by partnering with fintechs, embedding BaaS solutions in online retail offerings, and tapping the insights of agencies with big data expertise.

But it’s not enough to just add APIs. Consistent consumer experiences require new “omni-access” banking applications to a clean, highly available digital core. This is 80% of the battle.

What did you think?

Were there any key points I missed in the survey, or do you disagree with the findings? Either way, email me on [email protected] as I’d like to hear your thoughts.