Nigeria's Open Banking: A Technical Blueprint for CIOs and CISOs

- Isuru Wimalasundera

- Technical Lead, WSO2

The launch of Nigeria's open banking era is a mandate that is rapidly moving from a regulatory concept to a technical requirement. For CIOs and CISOs of Nigerian banks, this shift presents both a significant compliance challenge and a strategic opportunity. The primary concerns are maintaining security while exposing customer data, understanding the specific technology needed, and ensuring the investment delivers ROI are paramount.

This blog provides a technical blueprint, detailing the specific requirements of the Central Bank of Nigeria's (CBN) framework and outlining the foundational technology that turns compliance cost into a competitive advantage.

The mandate: From compliance to opportunity

Nigeria’s embrace of Open Banking addresses several pressing challenges, a considerable portion of the adult population are excluded from traditional financial services, and open banking would pave the way for broader financial inclusion by enabling fintechs to offer services like microloans and personalized budgeting. Open Banking would democratize credit access by allowing lenders to assess borrower behavior via comprehensive, consent-based data which fuels innovation and competition. By liberating financial data from institutional silos, empowering third-party developers to build tailored solutions which supports cross-sector integration, enabling telecoms, retailers, and others to embed financial services into daily life using standardized APIs.

Nigeria’s open banking ecosystem is governed by two key documents:

- The Regulatory Framework (2021), setting principles for API interoperability, risk-based access, and standardization. Link.

- The Operational Guidelines (2023), which detail technical requirements, security, governance, and operational rules. Link.

The latest updates about the Nigerian Open Banking can be found at https://openbanking.ng/.

Nigeria’s Open Banking framework is driven by seven key goals:

- Enable a modern regulatory environment that ensures secure, permission-based data sharing.

- Apply risk-based access tiers, governing who sees what level of customer data.

- Define clear roles and expectations for all ecosystem participants—including banks, fintechs, and third-party developers.

- Encourage competition and extend financial access, especially for underserved or unbanked populations.

- Ensure system stability & security through consent protocols, auditability, and robust API safeguards.

- Empower consumers with control over their own data and improve user experience.

- Standardize APIs to ensure seamless, secure integrations across providers.

The framework: Navigating tiers and trust

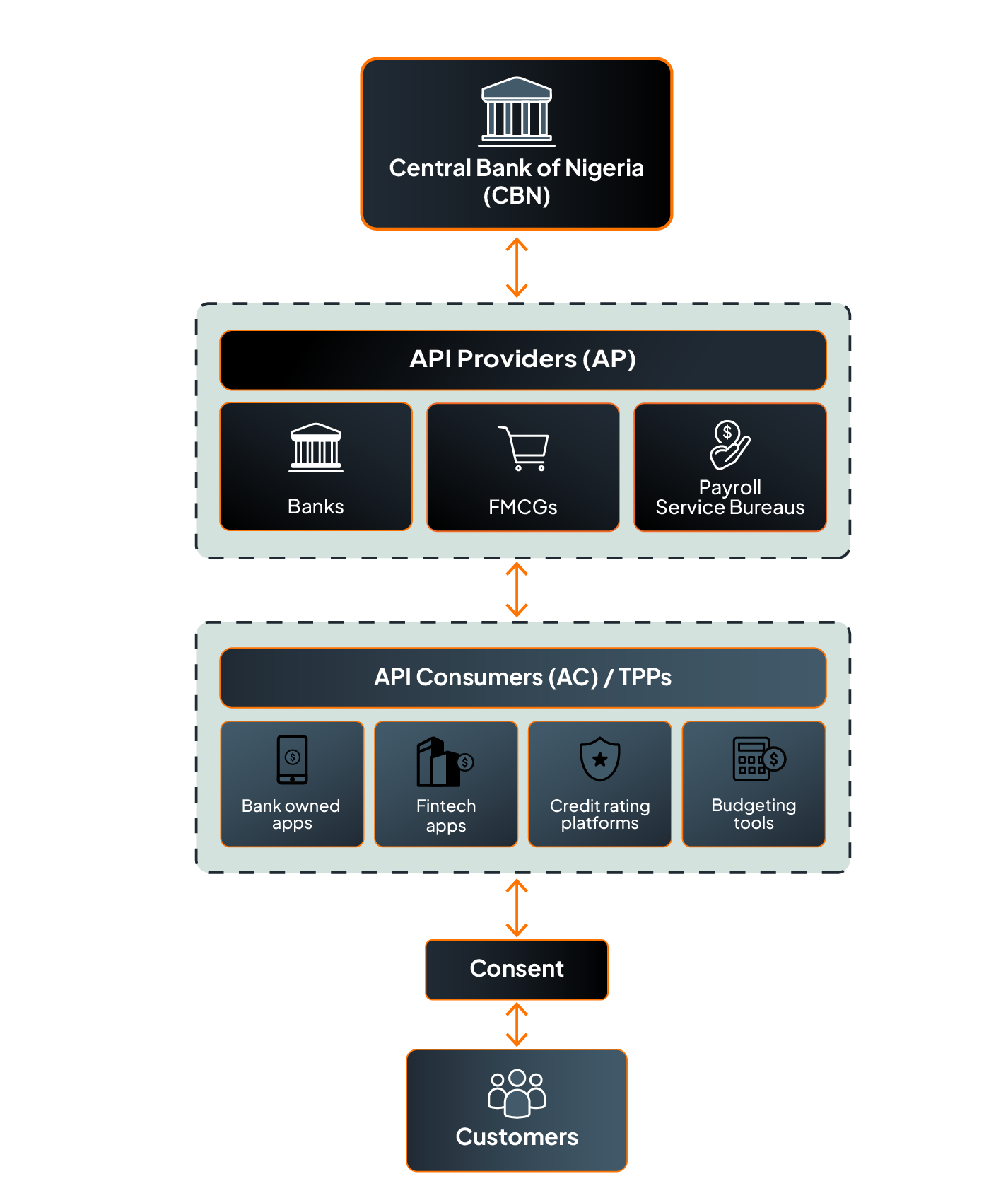

The Nigerian Open Banking Regulatory Framework introduces unique elements centered on governance, risk, and tiered access.

Core actors and governance

The ecosystem is governed by the Central Bank of Nigeria (CBN), ensuring compliance with legal, security, and technical standards.

The API Provider (AP) is usually a financial institution or a regulated entity that exposes APIs with customer data or services (e.g., account information, transaction history, payment initiation), for example Banks, Fast-Moving Consumer Goods (FMCG) companies, Payroll Service Bureaus.

The API Consumer (AC) is a third-party provider or financial institution that consumes the APIs exposed by API providers to offer new financial services. For example Bank-owned apps (Eg: Debt assessment apps / Client financial profiling apps), Fintech apps, credit rating platforms, budgeting tools.

And finally the customer, the owner of the financials and who provides consent to share the financial data.

Data & service categories

According to the CBN’s Open Banking Regulatory Framework, Open Banking participants exchange data via four tiered categories, each carrying different risk levels.

| Category Name | Description | Risk Level |

| Product Information & Service Touchpoints (PIST) | Data about financial products and access points (e.g., ATM/POS locations, fees, rates, channel URLs). Public-facing, non-sensitive information. | Low |

| Market Insight Transactions (MIT) | Aggregated, anonymized data such as transaction trends, customer behavior, and segment statistics. Not tied to individual users. | Moderate |

| Personal Information & Financial Transactions (PIFT) | Data at an individual customer level such as KYC details, account balances, transaction histories, and payment patterns. | High |

| Profile, Analytics & Scoring Transactions (PAST) | Sensitive analysis data like credit scores, income assessments, and other customer analytics. | High & Sensitive |

Risk management (RM) maturity levels & tier-based access

Nigeria’s Open Banking Regulatory Framework classifies participants into four tiers based on their RM maturity level, which determines their permitted data categories and required internal controls forming a “risk-tiered” model.

| Tier | RM Maturity Level & Requirements | Accessible Data Categories | Risk Level |

| 0 |

|

PIST, MIT | Low to Moderate |

| 1 |

|

PIST, MIT, PIFT | Moderate to High |

| 2 |

|

PIST, MIT, PIFT, PAST | Low to High & Sensitive |

| 3 |

|

PIST, MIT, PIFT, PAST | Low to High & Sensitive |

The technology: Foundational pillars for secure implementation

To comply with the CBN's operational guidelines and secure your data), a bank requires a platform that handles several specific, non-negotiable mandates.

Foundational API infrastructure

Nigerian banks must expose RESTful APIs using JSON or ISO 20022 payloads over HTTPS. This requires a robust API management platform to govern, secure, and monitor all digital services.

Strict security and consent mandates

Security requirements often exceed pre-existing measures. The platform must support:

- Security profiles: Stronger standards like Financial Grade API (FAPI) are mandatory, built on top of OAuth 2.0 and OpenID Connect.

- Encryption:Mutual TLS (mTLS) with TLS v1.2 is required for strong mutual authentication, and JSON Web Encryption (JWE) for message encryption.

- Data protection: Mandatory compliance with the Nigeria Data Protection Regulation (NDPR).

- Consent management: Consent must be explicit, replicating the format of the original agreement. It must be renewed annually or after 180 days of inactivity, and requires multi-factor authentication to guard against fraud. This necessitates a comprehensive Consent Management Platform.

Partner onboarding and interoperability

A key local nuance is that the Nigerian specification does not currently support automated Dynamic Client Registration (DCR). Instead, a manual Know Your Partner (KYP) due diligence process is mandated, requiring comprehensive risk assessments signed off by the Chief Risk Officer. The technology must facilitate this streamlined, yet controlled, Third-Party Provider (TPP) onboarding.

Performance and auditability

API Providers must provide performance monitoring dashboards accessible by API Consumers. Performance metrics must be sampled at intervals no greater than five minutes, and a summarized monthly performance report must be submitted to the CBN via the OB Registry APIs. This necessitates a platform with integrated Data Analytics and Insights capabilities.

WSO2 for Open Banking: Accelerating compliance and value

WSO2 Open Banking simplifies this complexity, offering a platform that is already deployed globally and pre-configured for standards like FAPI, ensuring accelerated compliance in Nigeria.

| CBN Requirements | WSO2 Open Banking Features |

| FAPI, mTLS, NDPR Compliance | Robust API Security & Standards Compliance: Full support for FAPI, OAuth 2.0, mTLS, and strong security profiles, ensuring comprehensive protection across all layers. |

| Explicit, Auditable Consent & Annual Renewal | Comprehensive Consent Management: A fully featured, CBN-aligned module enabling secure consent capture, lifecycle tracking, revocation, and audit dashboards. |

| Manual KYP Onboarding (No DCR Support) | API Onboarding & Developer Portal: Customizable developer portal and streamlined TPP onboarding workflows essential for managing tiered access and manual KYP requirements. |

| Integration with Legacy Systems | WSO2 Integrator Suite: A Modular Integration Layer that bridges modern APIs with legacy core banking systems (e.g., ISO 20022/REST/SOAP), crucial for efficient, non-disruptive implementation. |

| Mandatory Performance Reporting | Data Analytics & Security Analytics: Built-in capabilities to monitor, analyze, and log all transactional data, supporting CBN's monthly reporting and audit requirements. |

The future: Unlocking competitive advantage and ROI

Open Banking in Nigeria is not merely a technical directive; it's a profound opportunity for banks to unlock new strategic value. By moving beyond a compliance-only mindset, financial institutions can transform foundational technical requirements into powerful competitive advantages. The foundational components needed for compliance—robust API management, secure consent frameworks, and seamless integration layers—become strategic assets that enable banks to drive new revenue streams through monetization of their data, enhance operational efficiencies by automating data-intensive processes, and future-proof their digital infrastructure for ongoing innovation with AI/ML integration and microservices.

By embracing this transformation and partnering with strategic vendors like WSO2, who possess global expertise in this domain, banks can accelerate their journey. This allows them to focus on the business of innovation rather than the complexities of compliance, ensuring they not only meet the mandate but also build a scalable platform for future growth.

Within this strategic transformation, the IT department emerges as the key architect and enabler of this vision. By expertly navigating the technical requirements and building a secure, scalable platform, the IT team transitions from a cost center to a vital driver of innovation and business value. This is their moment to shine, laying the groundwork for a more dynamic and competitive future for the bank.

Ready to Unlock Your Bank's Open Banking Potential? Request Your Personalized Demo.